Banking Risks Management Systems

Methodology, business requirements, “turnkey” implementation

-

100%

Adjustment in compliance with the requirements of Central Bank -

BASEL II,III

Adjustment in compliance with the standards -

ALM

Liquidity management -

IFRS 9

Valuation of financial assets and financial liabilities, Impairment (Provisions), Hedging -

ANTI-FRAUD

Analytics to identify fraud and anti-money laundering typologies

Increasing of transparency and management of credit and operational risks

Control and forecasting of a market risk. Market risks connection with credit and operational risks

Forecasting and management of a Bank soundness

Reduction of time and costs for a manual reporting

Solution structure

The solution covers every function of the risk management and regulatory reporting of IFRS 9

Liquidity management

-

-

Calculation and report on interest risk (IRR report)

Supporting of stress tests, using the movement of curves of interest rates Supporting of stress tests, using the behavior models

-

Calculation and reporting on the liquidity gap (Liquidity GAP Report)

Static and dynamic report Support of changing business scenarios Support of the what-if analysis

-

Calculation and report on a cash flow

Intrinsic Liquidity Report or Cash-Flow report)

INTEGRAL RISK MANAGEMENT

-

Credit risk

Calculation of definitions of the codes used in calculation of statutory ratios N6, N7, R25. Calculation of repurchase transactions (Repo) and derivative financial instruments (Derivatives) CCR calculation (Basel II – CCR-Current Exposure Method)

-

Operational risk

Calculation of operational risks by Basic, ASA and AMA approaches

-

Market risk

Calculation of market risks (Market risk – The standardised measurement method) on a daily and monthly basis.

-

Standardized Approach/ IRB

Approach Calculation of a credit risk by Standardized Approach and Internal Ratings-Based Approach

Capital

-

-

Capital Calculation

Capital Calculation of capital components (B23 -Basel III) is made on a 3-level-basis Calculation of a countercyclical buffer to capital adequacy ratios (Basel III)

-

CVA Calculation

CVA Calculation (CVA - Basel III)

IFRS 9

-

The assets classification

Pre-configured assets classification

- Assets estimated by amortized cost

- Assets measured at fair value through other comprehensive income

- Assets measured at the fair value through profits and loss

Pre-configured models and SPPI tests

- Business model with a purpose of withholding of financial assets for getting cash flows in accordance with a contract

Possibility of models setting and alteration by Bank employees

- The test on compliance with criteria

- Entering of advanced option

-

Impairment

Customizing of the current Bank PD, LGD models or their creation

- Possibility of changing the amount of reserves via using different PD, LGD time horizons - On the horizon of 12 months - On the horizon of a transaction

- Consideration of macroeconomic factors’ influence in the models of defaults at calculations of reserve

- Setting of a transfer from TTC principle to PIT

- Unlimited amount of models

- Versioning models

- Changing of PD models under an amendment of macroeconomic parameters

- History of a depreciation in terms of portfolios and clients by the 3 stages of depreciation

- Preparation of accounting entries on the reserves bookkeeping for the transfer to further processing of Bank accounting systems

- Full cycle process of the calculation of impairment from the setting and management of the models to transferring of entries into accounting systems of the Bank

-

Hedge accounting

Calculation and verification of the fair value of financial instruments

- Calculation of the fair value of financial instruments

- Management of hedging relationships and monitoring of a hedge effectiveness

- Open and widening data model for support of a hedge accounting

Analytics to identify fraud and anti-money laundering typologies

-

Anti-Money Laundering (AML)

Checklists: Terrorist Financing Use of funds for illegal purposes

-

Know Your Customer (KYC)

Verification of your clients Customer identification (passport, TIN) Verification of listed addresses Verification of sources of funds Verification of inclusion in AML lists Risk analysis

-

Antifraud - checks

Monitoring and analysing suspicious transactions up to the moment of their execution Monitoring of suspicious transactions and transactions subject to mandatory control

-

Investigation of Payments

The search and investigation of customer payments when details are conflicting or unidentified

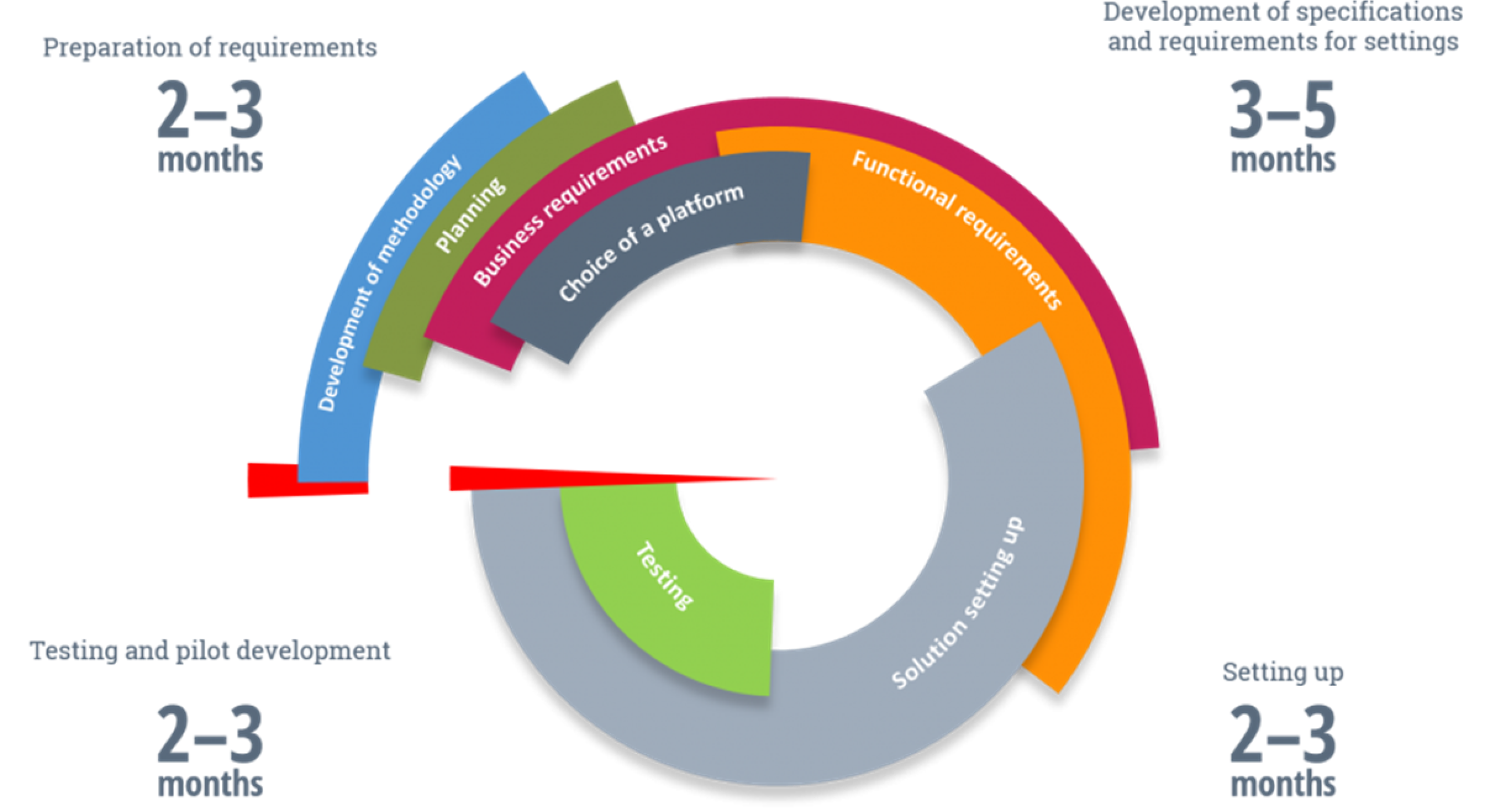

Implementation stages

Featured works

-

Building Business Information Management Systems

Building a data warehouse for a major bank, which entailed collecting business requirements, assessing task significance and complexity, deploying data marts, and implementing data quality control procedures.

-

Credit workflow for a Major Bank

Solution for automating crediting business processes, including portfolio management, marketing campaigns, and the entire lifecycle of credit applications and loans.